|

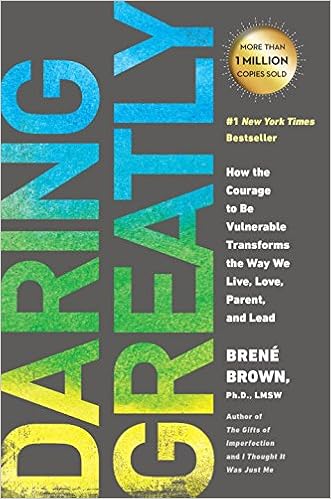

| Screen from Yahoo Finance. Annotations mine. |

The Buying

Back in September 2013, i bought Singpost at $1.26. Main reason was for the stable dividends that their cash flow could sustain. The rest of the numbers look okay too, including net cash position, growing businesses and that bit of eCommerce exposure. 4 years ago, eCommerce was growing massively which i felt could counter the weak domestic mail segment.

At that time, i just started dipping my toes into the markets and that position was about 25% of the capital then with 0 cash position in the portfolio. Definitely the newbie mistake of I can do anything thought.

Everything was stable and expected for a couple of quarters until 2nd quarter of 2014. Suddenly, price took a steep climb. I recall back then thinking that it was just sentiments and i should lock some profits when i could. Few days into that spike, i sold half my stake at $1.495 only to see a trading halt a week later. That's when Jack Ma's Alibaba took a stake.

I remember i was full of myself thinking that i was in before Jack Ma. How dumb. Because, the share price went up to almost $2 in October. That is a 40% gain that half of my stake missed out on. I felt so much regret in making that sell decision and that is the greed devil whispering into my left ear. The right ear was trying to console myself that i still have a stake that is now $2.

Piling on to that eCommerce story, i was convinced that Singpost is no longer just a stable company. It actually has a growth story especially with Alibaba backing them up. The voice in the head became - let's just hold on to this permanently. Anyway, the dividends are still coming, my cost is low so i have ample time to disembark this ship with a profit regardless.

It seems like nothing could go wrong and share price marked a high of $2.16 in January 2015.

Then, the oil crisis kicked in and the share price corrected together with the market. It was only until early Nov 2015 with the quarterly results coming in that i first spotted red flags. The company was struggling to grow the revenue despite rapidly rising cost. The net cash buffer dropped big time and i remember looking at it a bit concerned. To be fair, it was still net cash at this point. But the market did not like it as much and sent it way down.

Dividends are still maintained so i held on but i felt really bad for all the profits that i "returned" to the market.

CEO Resigns

Out of the blue, the CEO quits citing new endeavors. After a series of acquisitions, it felt to me like this company is next to get the typical CEO treatment. Two weeks later, we get announcements about corporate governance issues. Putting two together, it seems the new endeavor of his includes escaping a sinking boat.

That pulled share price way down to $1.335. Looks like back to square one for me.

And then the results came in Feb 2016. Everything was growing as they say in the slides but BAM! Net debt. Obviously the cost of driving all those growth is getting to them which derived less performance than they saw.

However, the share price rose for the next quarter, probably in-line with a recovering market. It rose to $1.60 and on hindsight, this is probably my last chance to escape, especially with that damning report coming from the corporate governance scandal.

I waited another quarter for the next results and it came out bad. eCommerce segment underperformed and underlying net profit actually fell.

I finally sold in July 2016. At the same price i did in May 2014. $1.495. Grand total of 2 years wasted there.

Takeaways

I made 2 selling decisions in this trade. One was probably too early. The other was probably too late.

I probably should have waited a bit more on the first sell because the momentum is to the upside. If others buy on rumors and sell on news, i probably could wait until at least the real news comes out before making that decision. Also, at $2, it is definitely not a price i would buy Singpost even with the kind of growth story. If it is not a price i would consider buying, i should seriously consider selling.

On the other hand, on the break of the corporate governance news and especially with the CEO resignation. The flags are waving in my face. To have a cash company going to debt, with an ongoing scandal, with people questioning about overpaying for acquisitions in May 2016, i think it is clear as day to bail. I could have also sold at the low too assuming i sell on the news, but if it recovered with weak fundamentals, i ought to have considered dumping at a price maybe slightly upwards of $1.50 which i had ample opportunities to.

It is painful to watch an opportunity go by and not participating in it. But it is equally or more painful to give back all the profits that you could have gotten back to the market. I definitely could have done better here.

Have an exit strategy to protect your profits.